Dear MPW Shareholders and Stakeholders,

MPT was founded more than 20 years ago to address a critical need. Hospitals are capital intensive, often requiring $1 million to $3 million per bed to construct – which is before taking into consideration required investments in critical medical equipment, information technology and operating costs. Compounding this challenge, hospitals have historically lacked access to many of the conventional funding sources that are prevalent across other sectors of the economy, particularly for their land and buildings.

In 2004, MPT began providing sale/leaseback capital to hospitals, providing funds for the acquisition, development and construction of about a half-dozen facilities. Since then, we have provided more than $22 billion of capital to more than 500 hospitals across the U.S. and nine other countries. Because hospital operators have had access to this capital, they have been able to grow and treat hundreds of thousands of patients. We are extremely proud of the role we have played in facilitating healthcare delivery in communities around the world.

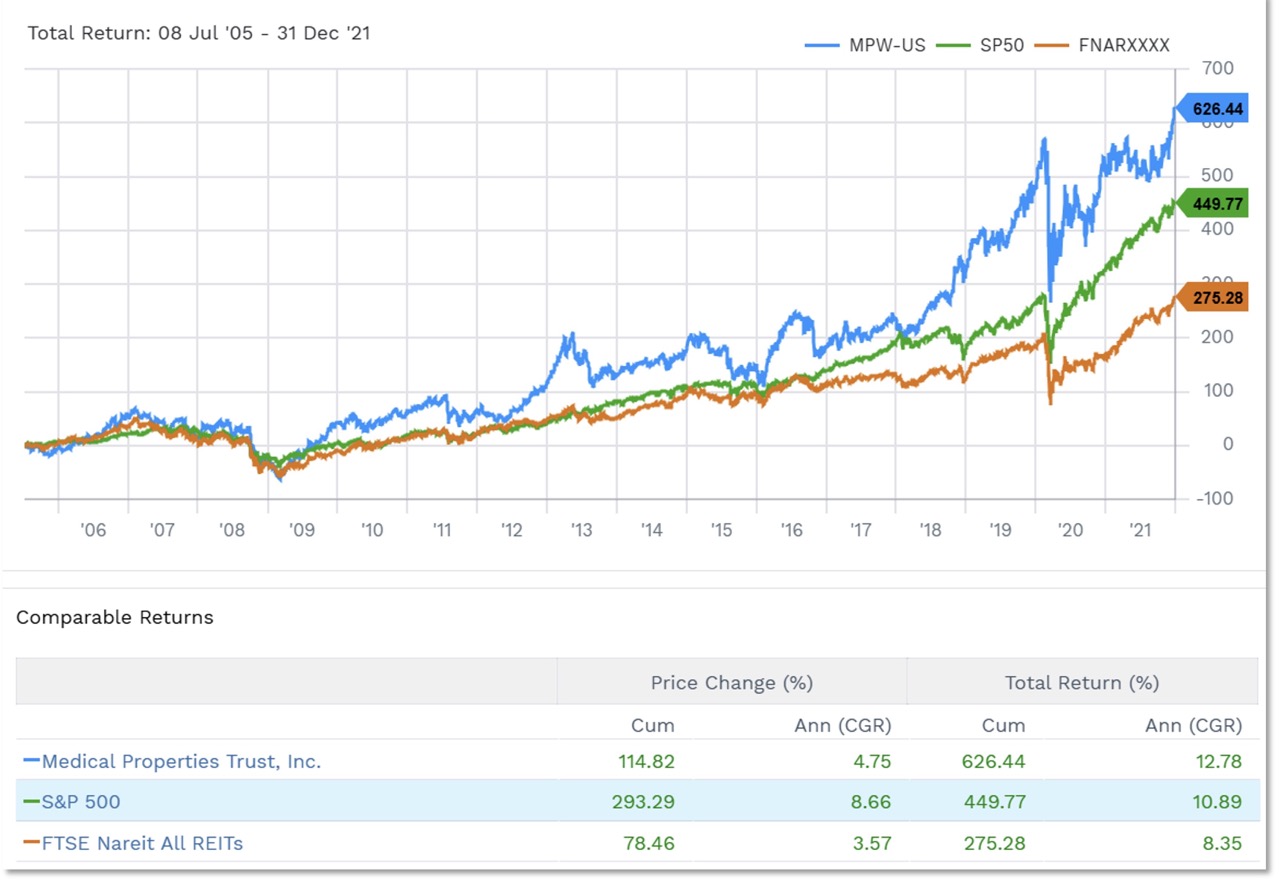

For most of our history as a public company, we generated outsized returns for our investors, including individual beneficiaries of and investors in many of the world’s largest state retirement systems, foundations, and endowments. In fact, from the time of our IPO in July 2005 through year-end 2021, we delivered 626% in total shareholder returns, significantly outperforming the S&P 500 and FTSE Nareit index.

Beginning in 2022, MPT came under a coordinated attack from a group of short sellers seeking to drive down our share price. These short sellers proved adept at working with the media to amplify their false claims; often enlisting politicians and organizations that are ideologically and unalterably opposed to private funding of the U.S. hospital business. The assertions about our business often lacked logic or even common sense, which would have been evident with a basic examination of the public record. We engaged in good faith over many months with analysts, government officials, activists and news organizations. Unfortunately, we learned first-hand that once a “narrative” is created, subsequent reporting and public commentary accept the original erroneous assertions as undisputed facts.

At various points over the past few years, we have attempted to fight back. In February 2023, the Audit Committee of our Board of Directors engaged Wachtell, Lipton, Rosen & Katz ("Wachtell Lipton") to conduct an independent investigation into these short selling firms’ claims. In addition to other findings, and with the assistance of a leading global consulting firm hired by Wachtell Lipton to assist with financial forensics, this independent investigation identified no evidence that MPT gratuitously overpays for real estate and no evidence of “round-tripping” of funds. A U.S. District Court Judge recently dismissed a proposed class-action lawsuit in which the plaintiff attempted to recycle these and other short seller arguments.

Unfortunately, the bankruptcies of two of our larger tenants – Steward Health Care and Prospect Medical Holdings – have emboldened our critics during this period. There are two key points that these critics consistently miss when talking about these two situations:

1. MPT’s sale/leaseback financing was utilized by both operators to replace more expensive short-term debt and other high-cost financing. The sale-leaseback transactions did not create a new cost out of thin air for these hospitals.

2. Rent was not the cause of financial distress. Months before its bankruptcy filing, Steward disclosed that its financial stress was created by, among other pressures, its failure to collect patient revenue from third-party payors. More specifically, on day one of its bankruptcy, Steward told the Court that patient mix, lagging reimbursement rates, declines in patient visits and revenues, a tightening labor market and sharp increases in labor costs were the root causes of distress. Rent expense was not even mentioned.

Similarly, rent was not mentioned when Prospect described the conditions leading to its bankruptcy; instead, liquidity challenges resulting primarily from stalled sales processes across various East Coast markets were the primary factors.

Notably – and evident in the public record – neither operator paid rent during lengthy periods ahead of their bankruptcy filings. In other words, these operators failed even with little or no rental expense. There is an opinion held by some that only government-funded and managed healthcare should be permissible in the United States. Even with the financial pressures Steward and Prospect suffered, there were alternatives to the courses taken in bankruptcy. However, at several turns, ideological and political considerations interfered and resulted in more disruption to hospital-dependent communities than was necessary.

The healthcare system needs and deserves the same capital flexibility afforded to other sectors of the economy. And MPT’s investors deserve the objective truth.

We are taking this opportunity to Correct the Record about our business. In the pages that follow, we will cover:

Disclaimer: This letter is being furnished solely for the purpose of responding to and correcting inaccurate, incomplete, or misleading statements made by third parties concerning Medical Properties Trust, Inc. (“MPT” or the “Company”). Investors are encouraged to review the Company’s filings with the Securities and Exchange Commission (the “SEC”), including its most recent Annual Report on Form 10-K and Quarterly Reports on Form 10-Q, for complete information about the Company and its financial condition.

References to third-party statements, media reports, or analyst commentary are included solely for context and do not imply that the Company adopts, endorses, or concurs with any such third-party information, conclusions, or opinions. The Company undertakes no responsibility for statements made by persons or entities not affiliated with MPT.

This material is not intended to be, and should not be construed as, an offer to sell or a solicitation of an offer to buy any securities of the Company. The information provided herein reflects MPT’s views, assessments, and understanding as of the date of this letter. MPT disclaims any obligation to update or revise the statements contained herein as a result of new information, future developments, or otherwise.